Venugopal Manghat is the Chief Investment Officer (CIO) - Equity of HSBC Mutual Fund. Venugopal was previously Head - Equity Investments, L&T Investment Management Limited from May 2016 to Nov 2022 and was Co-Head - Equity Investments, L&T Investment Management Limited from Apr 2012 - Apr 2016. Prior to 2012, he was Co-Head - Equities, Tata Asset Management Limited, India from 1995 - 2012. His educational qualification is MBA Finance, B.SC (Mathematics).

Answer :

Indian equity markets corrected 14% from October 2024 to February 2025 driven by slowdown in domestic economy and global concerns, resulting in lower earnings growth for FY25. Since March 2025, equity markets have posted 8% returns. The recovery has been driven by improving domestic economy conditions on the back of better liquidity conditions, lower inflation, bumper Rabi harvest, rate cuts by RBI and resumption of central government capex. However, the global economic scenario remains in a state of flux with concerns over slowing US economic growth, weakening dollar, rising treasury yields and tariff uncertainty. While we believe India is relatively better placed among global peers, there may be a possibility that the market may consolidate in a range for some time, until the global uncertainty settles down.

Answer : India's global manufacturing share stands merely at 2.7% vs China's share of more than 30%. Globally, many countries and companies had started to reduce their dependence on China and diversify supply chains, especially post disruption during Covid.

While it is too early to comment on how Trump tariffs will impact China, we see countries looking to enter more bilateral deals and moving away from China. Consequently, India becomes a great alternative destination driven by favourable demographics, labour cost advantages, government initiatives such as Make in India, Production-Linked Incentives (PLI) and improving ease of doing business.

We see some companies in the electronics, capital goods, textiles, auto, etc. may being beneficiaries of this diversification. Foreign investors may also show more interest in Indian equity markets driven by this diversification benefit.

While it is too early to comment on how Trump tariffs will impact China, we see countries looking to enter more bilateral deals and moving away from China. Consequently, India becomes a great alternative destination driven by favourable demographics, labour cost advantages, government initiatives such as Make in India, Production-Linked Incentives (PLI) and improving ease of doing business.

We see some companies in the electronics, capital goods, textiles, auto, etc. may being beneficiaries of this diversification. Foreign investors may also show more interest in Indian equity markets driven by this diversification benefit.

Answer : We see the following sectors most attractively placed over the medium-term:

Consumer Discretionary: As India's per capita income keeps increasing, we see consumption, especially, discretionary consumption to outperform the broader markets. The key drivers to this out-performance should be increased formalization, urbanization, digitization and convenience.

Financials: India has a fast-growing high net worth individual (HNI) and ultra-high net worth individual (UHNI) base driving investments outside the traditional asset class of bank deposits. The theme is clearly playing out with mutual funds garnering 20%+ growth over the past 10 years. Further, with resumption of RBI rate cuts, improving liquidity conditions and concerns on deposit growth abating, NBFCs and banks should also perform well.

Capital Goods: We are positive on the domestic manufacturing and Capital Goods sector may be a major beneficiary. The government has taken various initiatives such as PLI incentives, lowering corporate tax rates, GST and ease of doing business over the past years. These measures coupled with tailwinds in terms of China + 1 policy, favourable demographic and cost advantages in terms of labour, we see domestic manufacturing as a multi-year theme.

Infrastructure: The government has a keen focus on building the supply side of economy and remains committed towards investment in roads, railways, metros, ports, airports and defence. We see Power as a key multi-year theme with rising peak power deficits. We see considerable capex growth coming from the Power T&D segment and expect to see healthy order flows and activity from the sector.

Consumer Discretionary: As India's per capita income keeps increasing, we see consumption, especially, discretionary consumption to outperform the broader markets. The key drivers to this out-performance should be increased formalization, urbanization, digitization and convenience.

Financials: India has a fast-growing high net worth individual (HNI) and ultra-high net worth individual (UHNI) base driving investments outside the traditional asset class of bank deposits. The theme is clearly playing out with mutual funds garnering 20%+ growth over the past 10 years. Further, with resumption of RBI rate cuts, improving liquidity conditions and concerns on deposit growth abating, NBFCs and banks should also perform well.

Capital Goods: We are positive on the domestic manufacturing and Capital Goods sector may be a major beneficiary. The government has taken various initiatives such as PLI incentives, lowering corporate tax rates, GST and ease of doing business over the past years. These measures coupled with tailwinds in terms of China + 1 policy, favourable demographic and cost advantages in terms of labour, we see domestic manufacturing as a multi-year theme.

Infrastructure: The government has a keen focus on building the supply side of economy and remains committed towards investment in roads, railways, metros, ports, airports and defence. We see Power as a key multi-year theme with rising peak power deficits. We see considerable capex growth coming from the Power T&D segment and expect to see healthy order flows and activity from the sector.

Answer : We believe the fundamentals of the India long-term growth story continues to remain intact and the economy remains in an expansion phase. India has a strong domestic growth story, favourable demographics, government support for manufacturing and digital adoption. Over the next 5-10 years, India is likely to see steady growth in earnings and stock market performance.

Indian equity markets have been one of the best performing equity markets delivering mid-teens returns over the past decade or so. We see India's relative global attractiveness to remain intact over the coming years and advise long-term equity investors to remain firmly invested.

Indian equity markets have been one of the best performing equity markets delivering mid-teens returns over the past decade or so. We see India's relative global attractiveness to remain intact over the coming years and advise long-term equity investors to remain firmly invested.

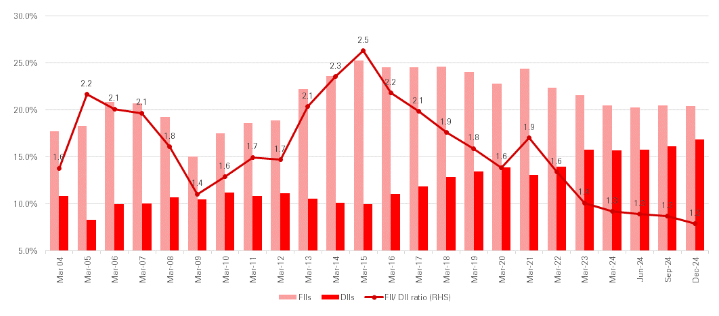

Answer : FII ownership in Indian equity markets has been continuously trending down from a high of 25.3% in March 2015 to 20.4% in Dec 2024. On the other hand, DII share is at an all-time high of 16.9% in Dec 2024 led by higher ownership of mutual funds. Accordingly, FII/ DII ownership ratio is at multi-decadal lows in Dec 2024 (see chart below). With healthy domestic flows continuing, we expect FII influence to keep coming down.

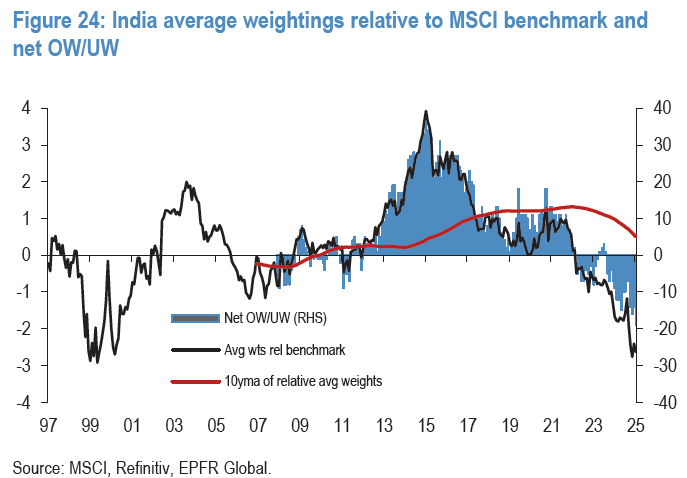

The recent inflows by FIIs is a reflection of India's high underweight position in Emerging Markets (see chart below). India's weight relative to benchmark (MSCI Emerging Markets Index) is at multi-decade lows offering attractive risk-reward for FIIs. Further, India's external situation remains fairly strong with $680 bn+ foreign exchange reserves. While FII flows may remain volatile over the short-term driven by the global uncertainty, currently India offers the best relative attractiveness for FIIs from a long-term perspective.

The recent inflows by FIIs is a reflection of India's high underweight position in Emerging Markets (see chart below). India's weight relative to benchmark (MSCI Emerging Markets Index) is at multi-decade lows offering attractive risk-reward for FIIs. Further, India's external situation remains fairly strong with $680 bn+ foreign exchange reserves. While FII flows may remain volatile over the short-term driven by the global uncertainty, currently India offers the best relative attractiveness for FIIs from a long-term perspective.

India average weighting relative to MSCI benchmark and net OW/UW:

Answer : Post recent strong years of 7%+ GDP growth, we see GDP growth moderating to 6-7% in FY25/FY26. Further, the global volatile environment is creating high uncertainty. Accordingly, valuations have seen corrections across market caps.

Empirical evidence suggests that smaller companies have been found to do well in expanding economic cycles or when economic growth rates are rising, leading to higher earnings growth rates. Another advantage of small caps is that its universe is the largest and is continuously expanding with more stocks getting added, many in relatively newer and niche sectors. Since the economy is expected to compound in nominal terms at a fast pace over the next several years there will be opportunities for companies, especially the smaller ones to grow.

On a longer-term basis, therefore we continue to be of the view that smaller companies may generate better returns and alpha from the market. However, in periods of short-term uncertainty (similar to current one), large caps should outperform mid and small caps. Hence, we believe that an optimum mix of mid and small cap stocks in an equity portfolio is important for long-term wealth building in a growth-oriented economy like India.

Note: Views provided above are based on information in the public domain and subject to change. Investors are requested to consult their mutual fund distributor for any investment decisions.

Source: Bloomberg, MOSL & HSBC MF estimates as on April 20, 2025 end or as latest available.

Disclaimer: This document has been prepared by HSBC Asset Management (India) Private Limited (HSBC) for information purposes only and should not be construed as i) an offer or recommendation to buy or sell securities, commodities, currencies or other investments referred to herein; or ii) an offer to sell or a solicitation or an offer for purchase of any of the funds of HSBC Mutual Fund; or iii) an investment research or investment advice. It does not have regard to specific investment objectives, financial situation and the particular needs of any specific person who may receive this document. Investors should seek personal and independent advice regarding the appropriateness of investing in any of the funds, securities, other investment or investment strategies that may have been discussed or referred to herein and should understand that the views regarding future prospects may or may not be realized. In no event shall HSBC Mutual Fund/HSBC Asset management (India) Private Limited and / or its affiliates or any of their directors, trustees, officers and employees be liable for any direct, indirect, special, incidental or consequential damages arising out of the use of information / opinion herein. This document is intended only for those who access it from within India and approved for distribution in Indian jurisdiction only. Distribution of this document to anyone (including investors, prospective investors or distributors) who are located outside India or foreign nationals residing in India, is strictly prohibited. Neither this document nor the units of HSBC Mutual Fund have been registered under Securities law/Regulations in any foreign jurisdiction. The distribution of this document in certain jurisdictions may be unlawful or restricted or totally prohibited and accordingly, persons who come into possession of this document are required to inform themselves about, and to observe, any such restrictions. If any person chooses to access this document from a jurisdiction other than India, then such person does so at his/her own risk and HSBC and its group companies will not be liable for any breach of local law or regulation that such person commits as a result of doing so.

Investors are requested to note that as per SEBI (Mutual Funds) Regulations, 1996 and guidelines issued thereunder, HSBC AMC, its employees and/or empaneled distributors/agents are forbidden from guaranteeing/promising/assuring/predicting any returns or future performances of the schemes of HSBC Mutual Fund. Hence please do not rely upon any such statements/commitments. If you come across any such practices, please register a complaint via email at investor.line@mutualfunds.hsbc.co.in.

The above information is for illustrative purposes only. The sector(s) mentioned in this document do not constitute any research report nor it should be considered as an investment research, investment recommendation or advice to any reader of this content to buy or sell any stocks / investments.

Document intended for distribution in Indian jurisdiction only and not for outside India or to NRIs. HSBC MF will not be liable for any breach if accessed by anyone outside India. For more details, click here / refer website.

© Copyright. HSBC Asset Management (India) Private Limited 2025, ALL RIGHTS RESERVED.

HSBC Mutual Fund, 9-11th Floor, NESCO - IT Park Bldg. 3, Nesco Complex, Western Express Highway, Goregaon East, Mumbai 400063. Maharashtra.

GST - 27AABCH0007N1ZS | Website: www.assetmanagement.hsbc.co.in

Mutual Fund investments are subject to market risks, read all scheme related documents carefully. CL 2656

Empirical evidence suggests that smaller companies have been found to do well in expanding economic cycles or when economic growth rates are rising, leading to higher earnings growth rates. Another advantage of small caps is that its universe is the largest and is continuously expanding with more stocks getting added, many in relatively newer and niche sectors. Since the economy is expected to compound in nominal terms at a fast pace over the next several years there will be opportunities for companies, especially the smaller ones to grow.

On a longer-term basis, therefore we continue to be of the view that smaller companies may generate better returns and alpha from the market. However, in periods of short-term uncertainty (similar to current one), large caps should outperform mid and small caps. Hence, we believe that an optimum mix of mid and small cap stocks in an equity portfolio is important for long-term wealth building in a growth-oriented economy like India.

Note: Views provided above are based on information in the public domain and subject to change. Investors are requested to consult their mutual fund distributor for any investment decisions.

Source: Bloomberg, MOSL & HSBC MF estimates as on April 20, 2025 end or as latest available.

Disclaimer: This document has been prepared by HSBC Asset Management (India) Private Limited (HSBC) for information purposes only and should not be construed as i) an offer or recommendation to buy or sell securities, commodities, currencies or other investments referred to herein; or ii) an offer to sell or a solicitation or an offer for purchase of any of the funds of HSBC Mutual Fund; or iii) an investment research or investment advice. It does not have regard to specific investment objectives, financial situation and the particular needs of any specific person who may receive this document. Investors should seek personal and independent advice regarding the appropriateness of investing in any of the funds, securities, other investment or investment strategies that may have been discussed or referred to herein and should understand that the views regarding future prospects may or may not be realized. In no event shall HSBC Mutual Fund/HSBC Asset management (India) Private Limited and / or its affiliates or any of their directors, trustees, officers and employees be liable for any direct, indirect, special, incidental or consequential damages arising out of the use of information / opinion herein. This document is intended only for those who access it from within India and approved for distribution in Indian jurisdiction only. Distribution of this document to anyone (including investors, prospective investors or distributors) who are located outside India or foreign nationals residing in India, is strictly prohibited. Neither this document nor the units of HSBC Mutual Fund have been registered under Securities law/Regulations in any foreign jurisdiction. The distribution of this document in certain jurisdictions may be unlawful or restricted or totally prohibited and accordingly, persons who come into possession of this document are required to inform themselves about, and to observe, any such restrictions. If any person chooses to access this document from a jurisdiction other than India, then such person does so at his/her own risk and HSBC and its group companies will not be liable for any breach of local law or regulation that such person commits as a result of doing so.

Investors are requested to note that as per SEBI (Mutual Funds) Regulations, 1996 and guidelines issued thereunder, HSBC AMC, its employees and/or empaneled distributors/agents are forbidden from guaranteeing/promising/assuring/predicting any returns or future performances of the schemes of HSBC Mutual Fund. Hence please do not rely upon any such statements/commitments. If you come across any such practices, please register a complaint via email at investor.line@mutualfunds.hsbc.co.in.

The above information is for illustrative purposes only. The sector(s) mentioned in this document do not constitute any research report nor it should be considered as an investment research, investment recommendation or advice to any reader of this content to buy or sell any stocks / investments.

Document intended for distribution in Indian jurisdiction only and not for outside India or to NRIs. HSBC MF will not be liable for any breach if accessed by anyone outside India. For more details, click here / refer website.

© Copyright. HSBC Asset Management (India) Private Limited 2025, ALL RIGHTS RESERVED.

HSBC Mutual Fund, 9-11th Floor, NESCO - IT Park Bldg. 3, Nesco Complex, Western Express Highway, Goregaon East, Mumbai 400063. Maharashtra.

GST - 27AABCH0007N1ZS | Website: www.assetmanagement.hsbc.co.in

Mutual Fund investments are subject to market risks, read all scheme related documents carefully. CL 2656